Auctions and Tapers

Why interest rates will soon spike much higher

Summary:

As the Fed “tapers” – and especially post-taper in March – Treasury yields will spike much higher than markets now expect.

The reason: In 2021, the the Fed bought all of the $1 trillion in new debt issued by the Treasury. Private investors bought (net) zero Treasury debt.

Absent the Fed in 2022, private buyers will require much higher yields to induce them to absorb the entire $1 trillion in additional Treasury debt.

Keep an eye on Treasury auctions; the Fed will no longer provide a backstop for dealers.

Treasury Bond Auctions: Canaries in the Coal Mine

Stock market investors have seldom paid much attention to the regular Treasury debt auctions They have always seemed like the obscure mechanics of our regulatory plumbing. But over the next couple of months, it will be critically important for investors to pay close attention to these auctions and their results.

For the past decade, and especially over the past two years, Treasury auctions have typically gone off without a hitch. Newly auctioned Treasuries are bought, first, by private buyers and, second, by primary dealers (mostly, the large banks) who mop up those securities that the public doesn’t buy and put them in their investing and trading books.

“Quantitative Easing” meant that dealers bore minimal risk when bidding for bonds being auctioned. The Fed does not buy Treasuries directly in an auction. To fulfill QE objectives, the Fed must buy Treasuries from primary dealers in the secondary market. So dealers can bid aggressively for inventory in auctions, knowing that the Fed stands ready to buy when they want to sell. They can lose a little money, but there is no way they can take a real bath. The Fed’s constant presence as a buyer sets a floor on bond prices (that is, it prevents interest rates from going higher.)

Fed “tapering” is likely to throw a wrench into these auctions. QE will no longer compel the Fed to provide a backstop in the aftermarket.

Post-taper, the debt monster will awaken

There was a monster lurking beneath the placid surface of the 2021 Treasury auctions; in 2021, the Federal Reserve bought all new Treasury debt. Not in the auctions, but from dealers in the aftermarket. As QE subsides, private buyers will need to step in to supplant the Fed.

How can I assert that the Fed bought all new Treasury debt in 2021? Here is my reasoning: The U.S. Treasury’s financial position at the close of 2020 was an anomaly; its account at the Federal Reserve on Jan. 1, 2021, was a gargantuan $1.6 trillion. Having borrowed $4.5 trillion in 2020, the Treasury still had $1.6 trillion in cash left over at year-end.

Source: St. Louis Federal Reserve

In recent history, the Treasury account has typically ranged between $100 billion and $300 billion. It pretty much started the year and ended the year in the same place. Thus, traditionally, the Treasury had to borrow to fund its entire deficit. But in 2021, with a $1.6 billion head start, the Treasury borrowed $1.5 trillion or so less than they otherwise would have had to in a normal year.

By year end 2021, total Federal debt will have increased by “only” $1 trillion, even though the Treasury will have spent $2.6 trillion. This number is issued quarterly, so we only have numbers as of September 30 and must estimate the fourth quarter. In the first nine months, total debt increased $750 billion, so another $250 billion seems reasonable.

Source: St. Louis Federal Reserve

The Fed balance sheet will have increased by roughly $1.4 trillion in 2021. Extrapolating from third quarter numbers, the Fed will have bought $1 trillion in Treasury debt and $600 billion in agency MBS. (Certain other asset accounts declined slightly.) Thus, unless I am missing something, the Fed in 2021 will have purchased almost exactly as much Treasury debt as the Treasury issued. Private investors bought zero.

Source: St. Louis Federal Reserve

Private investors will demand much higher yields

Soon the Treasury and the Fed will confront a daunting challenge; in the Fed’s absence post-taper, they will need to persuade private investors to buy $1 trillion of additional Treasury debt (based on CBO budget projections) that these investors had summarily rejected at prevailing 2021 yields. How do they propose to accomplish this? There is only one way I know of.

There are always private market bidders in any given auction. Auctions are typically the cheapest source of bonds for investors who must buy bonds with longer maturities (foreign countries and central banks, pension funds, insurance companies, mutual funds, etc.) But overall, in 2021, private buyers bought zero Treasuries.

My working hypothesis is that intermediate to long term interest rates are set to spike sharply higher over the next year — far higher than the consensus now expects. It is difficult to imagine that $1 trillion worth of new buyers will magically appear at anything close to current interest rates, especially in light of recent inflation trends.

Sharply higher interest rates are likely to unsettle equity markets with a downward revaluation of many stocks. Watching CNBC, I am astounded by the inability of experts – even those I respect – to imagine that the 10 year Treasury yield might exceed 2.25%. This, with inflation now running north of 6%. None of them (with the possible exception of Rick Santelli) are in any way prepared for a 3-5% ten year.

Higher rates will eventually raise recession concerns that could further pressure the stock market, regardless of Fed actions at the short end. Credit issues will inevitably emerge, especially among the more highly leveraged firms and those that may not be generating positive cash flow.

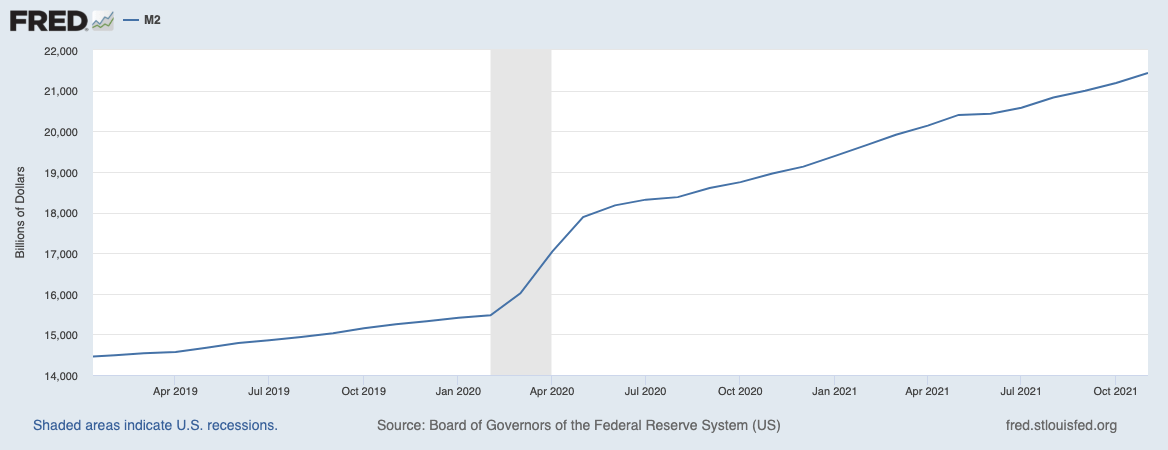

Whether inflation abates will depend on future money growth. Right now, M2 is still surging at a 10% annual rate, so serious inflation will be with us for a while. Unconscionably, the idea that it is excess money growth that drives inflation is anathema to most of today’s economists. As I argued in “Ain’t Nothin’ But A Party,” this is largely because monetarism is associated with Milton Friedman, who was not politically liberal and not a Neo-Keynesian. He was, however, right.

Our banking system could be an impediment to the Fed’s ability to control future inflation. Thanks to QE, banks are sitting on an immense endowment of free reserves (in 2020 the Fed changed its reserving policies and definitions, so I’m not 100% certain I am using the correct terminology.) If inflation continues or worsens, loan demand is likely to accelerate as firms seek to buy inventory and undertake projects in advance of higher prices. This, in turn, will create more money, and is beyond the Fed’s control absent credit restrictions.

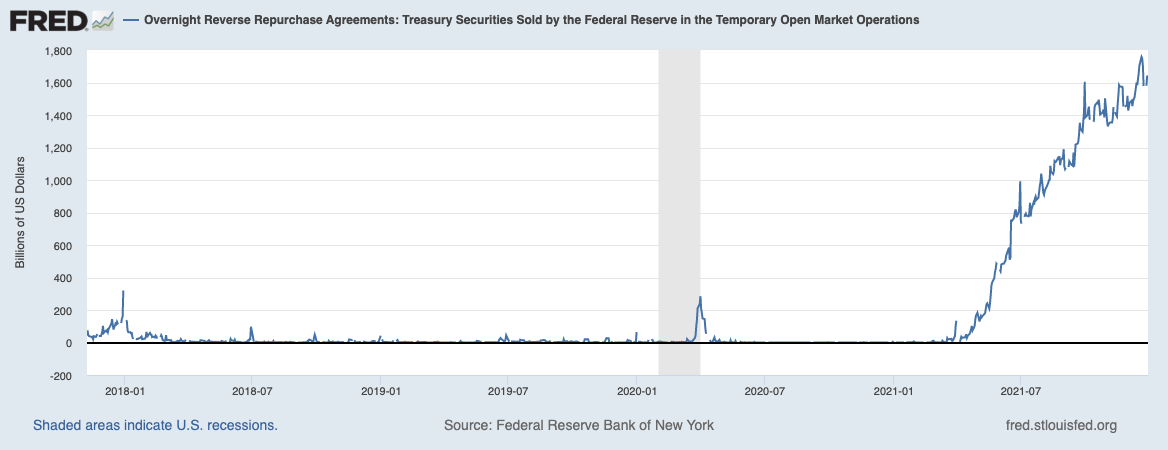

Currently, banks and MMMF’s are parking these balances at the Fed as Reserves and “Reverse Repos” because they have no better alternative. (And because the Fed is desperate to keep short rates positive.) Forget “lender of last resort,” the Fed is now “borrower of last resort.” Big time.

Source: St. Louis Federal Reserve

Source: St. Louis Federal Reserve